Categories:

Energy

Topics:

General Energy

Q1 Drilling Shows Patterson Lake Makes The Grade: Literally

Disclosure: I am long ESOFD.PK.

Patterson Lake Delivers in Q1/Q2: High Grade and Wide Open

So much has happened in the last two quarters, that a brief recap seems in order with respect to the Patterson Lake Uranium Project. The Fission Energy asset sale to Denison has now been completed and Fission Uranium has started trading as a new entity (FCU on the TSX Venture). Share price action has been volatile for both Fission and Alpha, with Fission trading as high as $1.25 before pulling back to the $0.95 level (Alpha Minerals traded as high as C$5/share before pulling back to current levels in the C$3.25 range) as the stocks consolidate the impressive gains seen over the last 6-9 months. At current levels, investors have far more data than they did at the beginning on the drill program which makes a review of the data even more important for existing and potential shareholders.

With less than half of the drill results from the winter program reported, and the summer drilling season fast approaching, 50/50 JV partners Fission Uranium (FSSIF.PK, new ticker needed) and Alpha Minerals (ESOFD.PK) have already delivered some of the highest grade-for-depth uranium intervals seen in the world in the last 30 years. Highlight intercepts in drill core include: 34 meters of 4.92% U3O8, 53 meters of 6.57% U3O8 (including 10.5 meters of 29.26% U3O8), and 49.5 meters of 6.26% U3O8 (including 6 meters at 35% U3O8).A total of 46 holes were drilled with 37 of those intersecting anomalous radioactivity and massive and/or disseminated pitchblende (uranium) mineralization for a success ratio of approximately 80%. The mineralization is being encountered starting at depths ranging from 60 to 100 meters, which is exceptionally shallow for a deposit of this grade (Hathor's Roughrider deposit was between 200 to 400 meters deep). This shallow depth has the potential to result in lower development costs, lower operating costs, and more favorable overall economics. In short, the results are nothing short of spectacular for a first-pass drill program.

The grades and thicknesses of uranium mineralization and alteration encountered thus far are suggestive of a long-lived and potentially large system. End-to-end, mineralization has been discovered along roughly 800 meters of strike length, and the deposit remains open to expansion in all directions. Radon gas analysis has been used as an indicator for underlying uranium, given that radon gas is a natural product of natural uranium decay. This "radon targeting" is innovative, and at least partially responsible for the high exploration success rate to date. Grades as high as 45% U3O8 have been encountered, which should catch the attention of even the most hardened mining investors. To put it bluntly, you just can't get 45% U3O8 into a rock unless the mineralizing system is long-lived. The accumulation of mineralization (be it gold, copper, or uranium in this case) takes time, so to see grades at high as those being seen at Patterson Lake, it is logical to assume that uranium-bearing fluids were pumping through the rock for a long time. These fluids moved through a network of interconnected fractures and fissures which has been shown to be mineralized over a strike length of at least 800 meters. In the uranium world, this already qualifies it as a large system and the high grades mean that the resource has the potential to grow quite quickly. If anyone is still wondering, both of these attributes are good signs for the forward program.

Hathor's entire resource (57 million pounds) at their Roughrider deposit (which was sold to Rio Tinto for C$654 (~$11 per pound of resource) in 2011) was contained within approximately 300 meters of strike length. This is not to say that the full 800 meter strike length currently outlined at Patterson Lake will be mineralized, but given that the zone is open at both ends and given the grades being encountered in drill core, the Roughrider comparison is certainly worth consideration when thinking about the potential that is on the table at Patterson Lake South.

In my opinion, only a handful of investors have grasped the potential significance of the results released to date, which I believe has created a favorable risk-reward profile for investors who can think even just a few months in advance. Based on analyst estimates published by Cantor Fitzgerald and Dundee Securities, the back-of-the-envelope math suggests a deposit in the 20-25 million pound range based on the existing data at Patterson Lake South. In the market (after adjusting for cash balances) the PLS project is currently valued at roughly C$130 million, which means that the market is currently valuing the PLS project at only $5-6 per "pound in the ground" on current data. Given that evidence thus far is suggestive of a large and long-lived mineralizing system (as discussed above), not only are investors getting exposure to PLS at roughly half the valuation per pound that Hathor was eventually sold for, but they are also getting any deposit expansion at little or no cost. In light of the success seen on the first-pass drill program, and the fact that the source of the boulder field still hasn't been found, it is highly unlikely that Fission and Alpha have found all the uranium there is to find at Patterson Lake.

Alpha and Fission currently have close to $40 million in cash combined, which is a veritable war chest with respect to the Patterson Lake project. When one considers that the entire 2013 winter drill program cost approximately $4-5 million for 10,000 meters of drilling, it's clear that this project is well-funded to say the least. By my estimates, the summer drill program should start by the first or second week of July, which is only 2 months away. This provides a relatively brief window for investors who agree with the thesis presented here to establish positions ahead of that drill program.

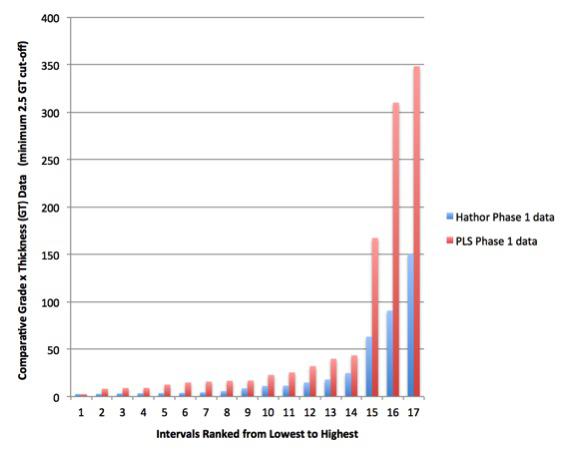

In terms of project valuation relative to Hathor at a similar stage of drilling, Patterson Lake now trades at roughly half of where Roughrider did despite the fact that the Patterson Lake drill data actually exceeds anything that Roughrider had at this stage (after its first winter drill program, the Roughrider project was valued at $230 million). Refer to my prior summary here of Hathor's valuation history. Below, I have presented a comparative bar chart of the drill results from each project to date for consideration in order to visually represent the data in terms of "grade thickness", which is found by multiplying the thickness of any given interval by its average grade in order to make quantitative hole-to-hole comparisons.

Figure 1: Comparative Grade-Thickness data from Patterson Lake and Roughrider

(click to enlarge) (Data source: Company reports)

(Data source: Company reports)

Summary

While it is no doubt early in the history of the Patterson Lake Uranium project, when the above information is itemized, the project clearly stands alone in the uranium market:

1. Results from the winter program have already defined a large, high-grade system with the potential for additional expansion.

2. The drill data looks excellent on its own or on a comparative basis, and the valuation is significantly lower than the most recent market comparable.

3. The balance sheets of the JV partners are strong and the summer drill program is likely only about 2 months from starting.

4. Patterson Lake stands on its own as the highest grade uranium discovery at its depth discovered anywhere in the world in the last 30 years.

Supply and demand fundamentals in the uranium market are generally well-known, with the nearest-term uncertainty being the restart of Japan's nuclear reactor fleet. General consensus is that at least some Japanese reactors will be restarted this year and there is broad agreement that the current energy situation in Japan is totally unsustainable (see links here and here). The Russian HEU agreement ends at the end of this year and mine development and expansion projects remain on the back-burner in light of the current price environment, suggesting there is really only one direction for uranium prices to go in the medium-term; which is higher.

Uranium has been best described as a "when, not if" trade, which is a view that I share. By the time the trade is "on" I fully expect that Patterson Lake will be trading at multiples of the current project valuation with even modest success in the forward programs given what has already been outlined. Both Alpha and Fission have the balance sheets to continue to move the project forward and all investors need is the foresight to see what the data is indicating. Eventual buying from the Global X Uranium ETF (URA) is all but a formality in my view, and the pending final closing of the Uranium One acquisition by ARMZ should be the catalyst which brings that ETF into the mix.

Before this winter's drill program, I had initially described the speculative nature of Patterson Lake as a bet at the racetrack. While still speculative to some degree, the risk appears to be decreasing consistently. There are no guarantees in the resource industry, but with grade, depth, scale, and comparative valuation all working together, I think this is about as good as it's ever going to get at this stage in the race.