Click here to read important disclaimer & disclosures Click here to see more about Gunnison Copper

America’s Newest Copper Producer

TSX: GCU | OTCQB: GCUMF

Disseminated on behalf of Gunnison Copper Corp.

Made-in-America Copper From the

Great State of Arizona

Johnson Camp Mine Now Producing — Supplying US Data Centers, Defense & Domestic Supply Chains with 100% American Copper

AMERICA’S NEWEST COPPER PRODUCER WITH TRUE DISTRICT-SCALE POTENTIAL

Now Producing with Control of Large Portion of Cochise Mining District, AZ

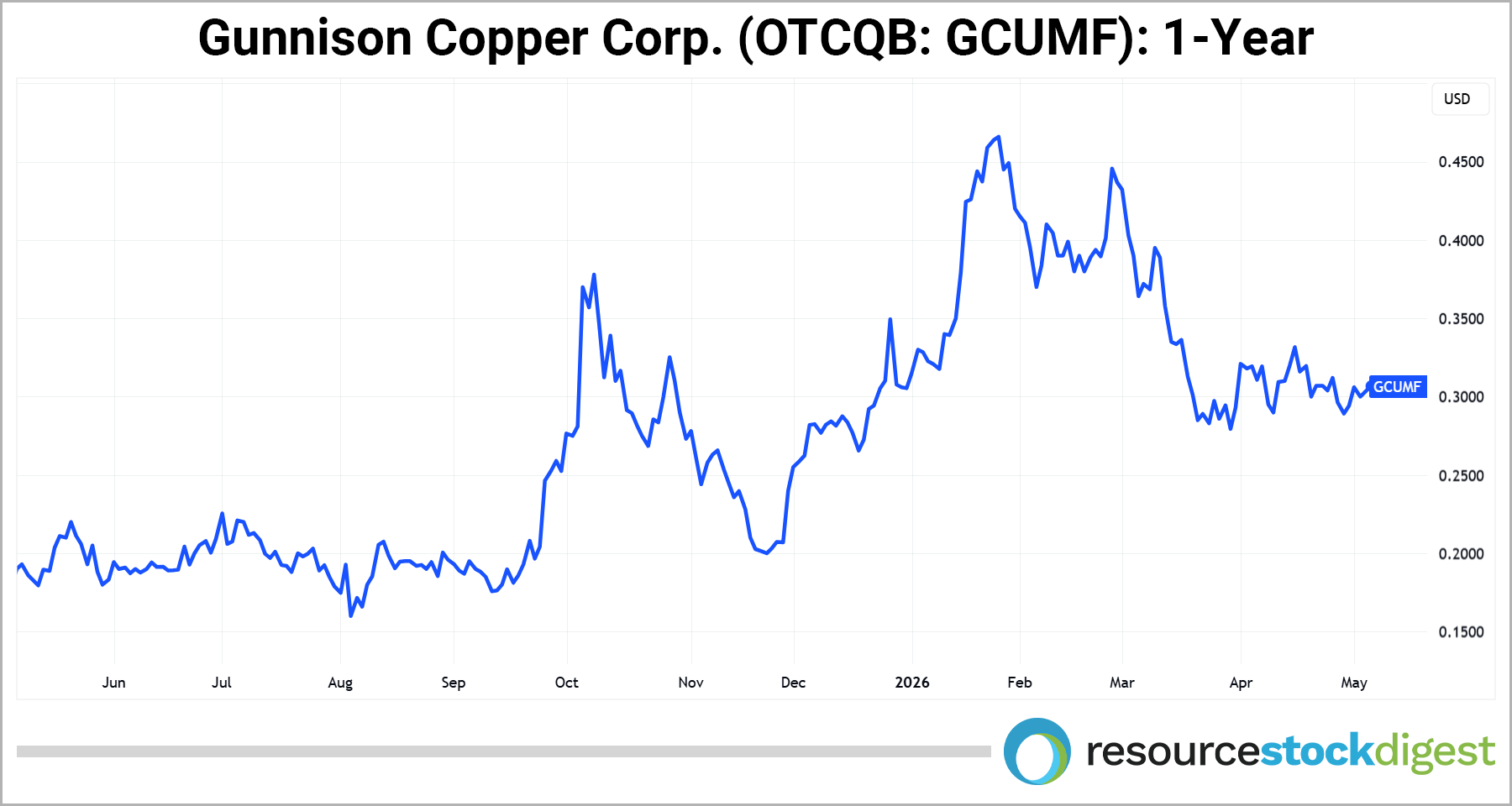

— Current Market Price ~ US$0.30 Per Share —

Click Here to Read Sponsor Disclosure

Gunnison Copper: Flagship Johnson Camp Mine, AZ

First Revenues Flow as Johnson Camp Delivers 100% USA Copper

Gunnison Copper Corp. (“GCU”) has achieved what few juniors ever do: first copper production and first sales.

With its Johnson Camp Mine now online in Arizona, GCU is delivering 100% Made-in-America copper straight into the US supply chain.

It’s a milestone worth celebrating — and now part of a much broader and rapidly evolving domestic supply chain story.

Why? Because Gunnison Copper controls a large portion of the Cochise Mining District — an established Tier-1 jurisdiction that has significant historical production.

With production and sales already underway — and every pound mined and processed in the United States — the scale of the opportunity is significant.

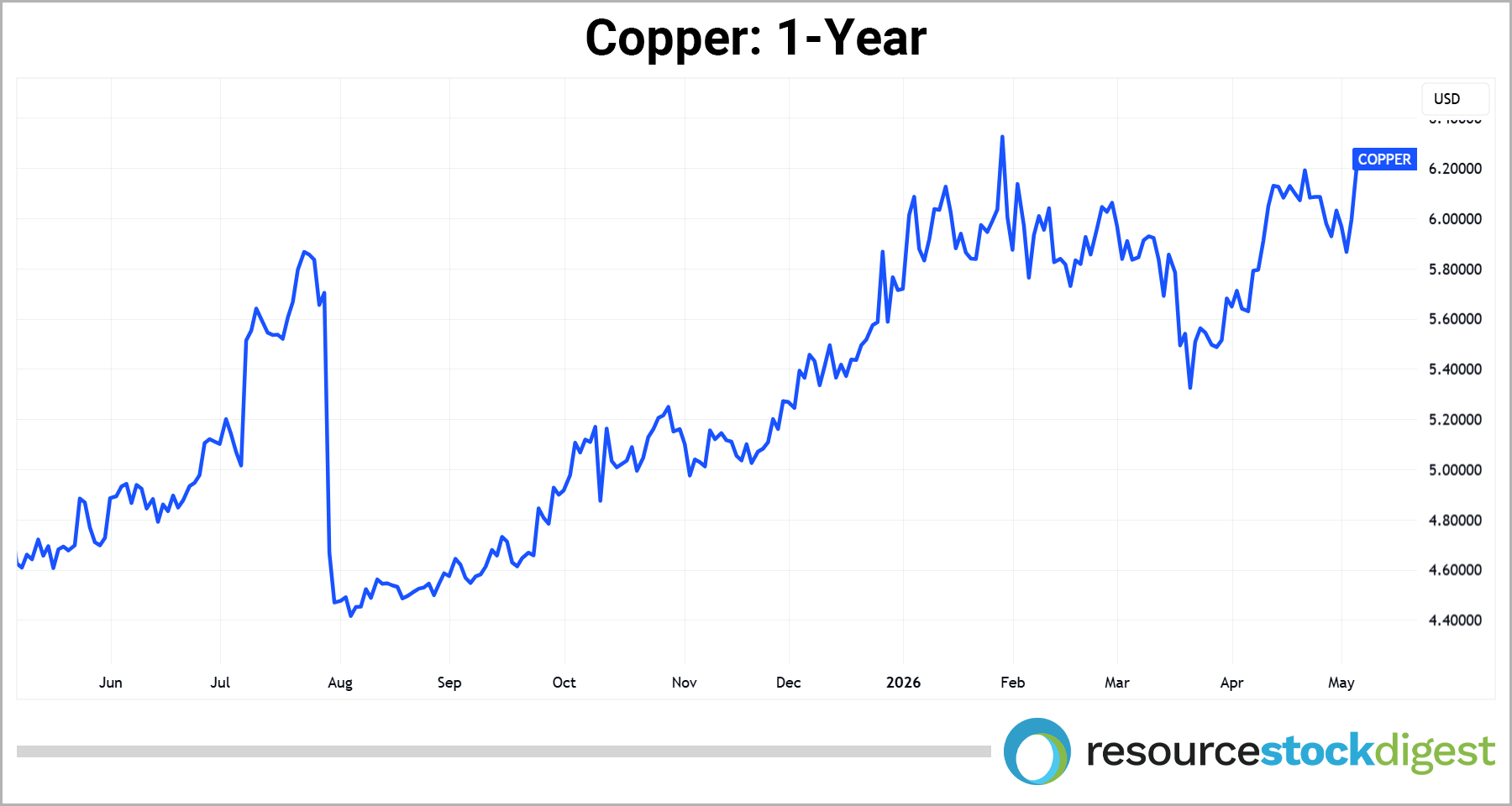

Layer in copper racing toward all-time highs above US$6/lb, supply shocks from the world’s second-largest copper mine in Indonesia, and a global commodity supercycle lifting all boats… and you’ve got the makings of an opportunity for investors to consider.

Importantly, that production is now beginning to connect directly to next-generation demand, including data centers, AI infrastructure, defense, and domestic manufacturing.

With shares still trading around US$0.30, despite major operational and strategic milestones, there is potential, and the America-first angle couldn’t be more timely. Of course, any mineral project is subject to risks related to permitting, financing, and execution that should be considered before making an investment decision.

So let’s dive in to see how these early milestones, combined with district-scale control and emerging strategic partnerships, could drive the next phase of growth.

Production Milestone Anchored by District-Scale Control

Johnson Camp 25M lbs/yr Production Capacity as

Gunnison Builds Out Cochise District

The significance of Gunnison Copper’s first production and sales milestone cannot be overstated.

In late August 2025, the Johnson Camp Mine (JCM) officially entered production ahead of schedule, buoyed by strong execution and an excellent health and safety record.

Within weeks, the company had delivered its inaugural 225,000 pounds of copper cathode into US markets, generating over US$1M in gross proceeds at an average realized price of US$4.64/lb.

The first sale was recorded on September 15, 2025, marking the start of recurring cash flow from JCM that will be used to pay down funds advanced by Rio Tinto’s Nuton® venture.

For Gunnison Copper director Dr. Stephen Twyerould, the achievement is more than just a technical milestone — it’s proof that responsible American copper production can be delivered ahead of schedule with safety and ESG commitments firmly in place.

For Craig Hallworth, President & CEO of Gunnison — whom you’ll be hearing from directly in our exclusive interview just ahead — those first sales represent not only the start of production but also the beginning of a rerating opportunity as Gunnison transitions into the ranks of bona fide copper producers.

Importantly, JCM isn’t a small-scale pilot project — it’s backed by Rio Tinto’s Nuton® venture and built for scale with a nameplate capacity of 25 million pounds per year of 100% Made-in-America copper.

In January 2026, Rio Tinto’s Nuton® venture announced a strategic collaboration with Amazon Web Services that will see the first Nuton copper produced at Johnson Camp used in AWS’s US data centers, while integrating cloud-based analytics to accelerate optimization of the bioleaching process.

As noted, every pound is mined and processed within the United States, expected to directly support energy independence, advanced manufacturing, technology, and national defense supply chains.

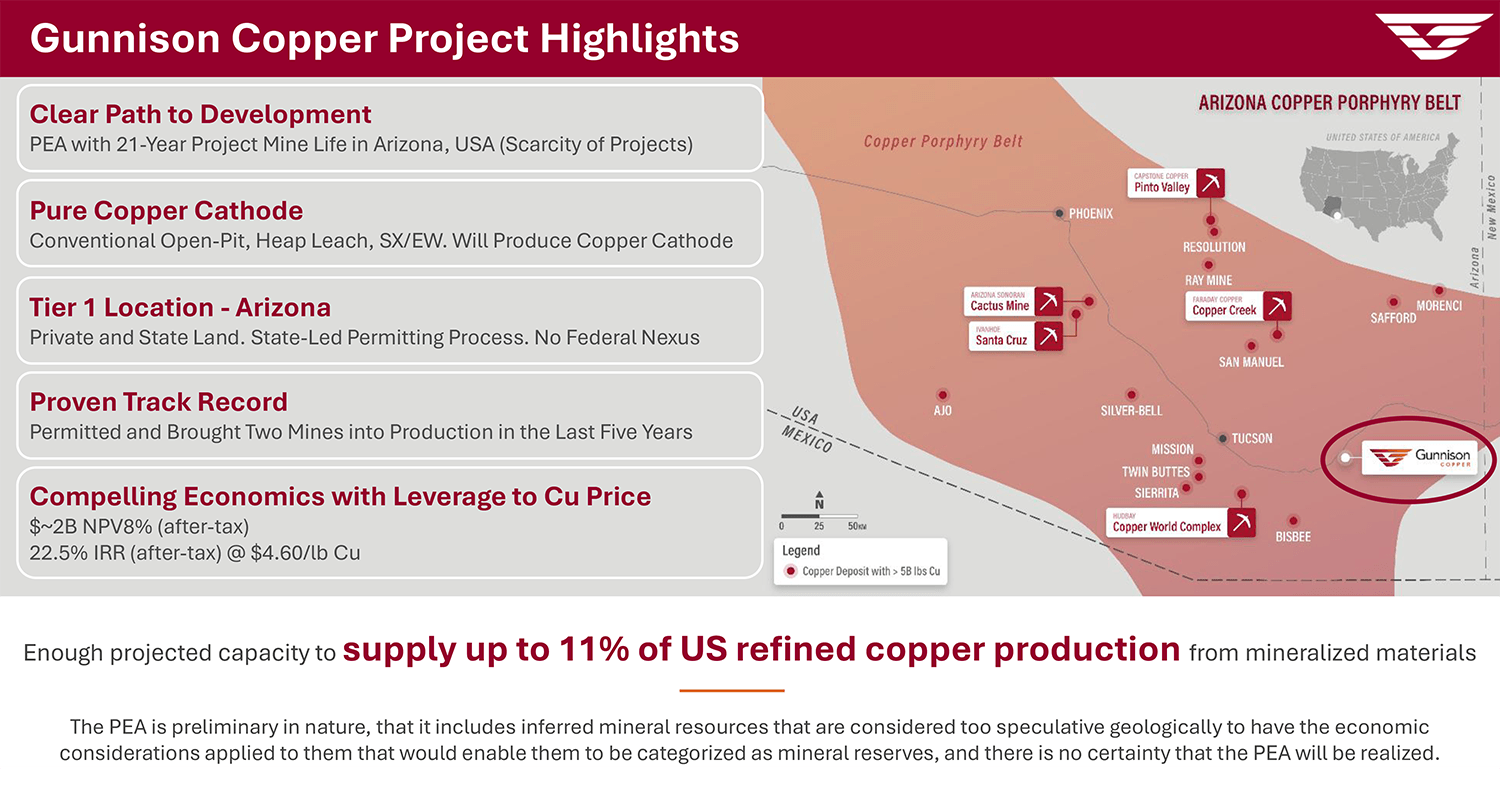

Beyond Johnson Camp itself, Gunnison’s advantage lies in control of a large part of the surrounding Cochise Mining District — a historic copper camp with 12 known deposits spread across an 8 km corridor.

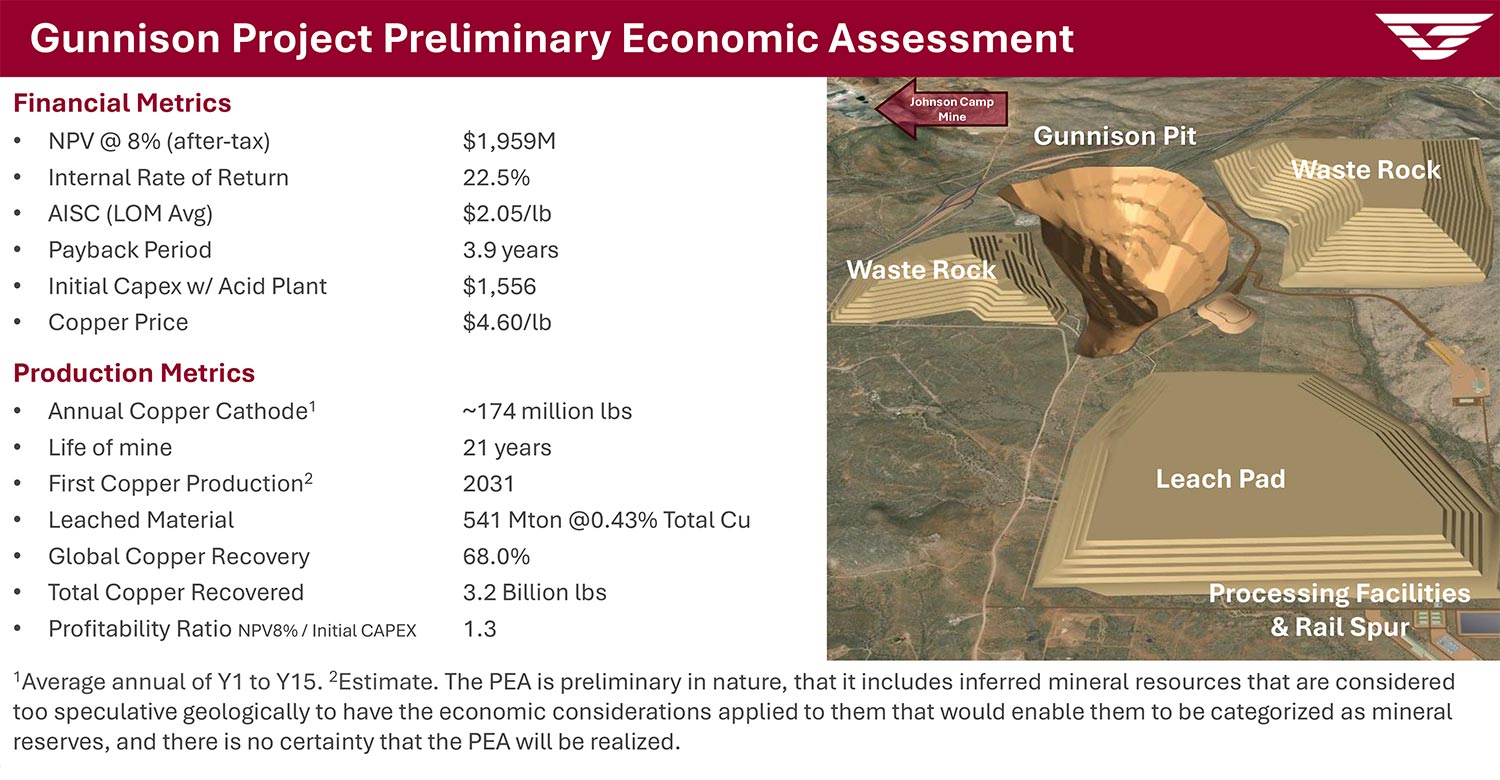

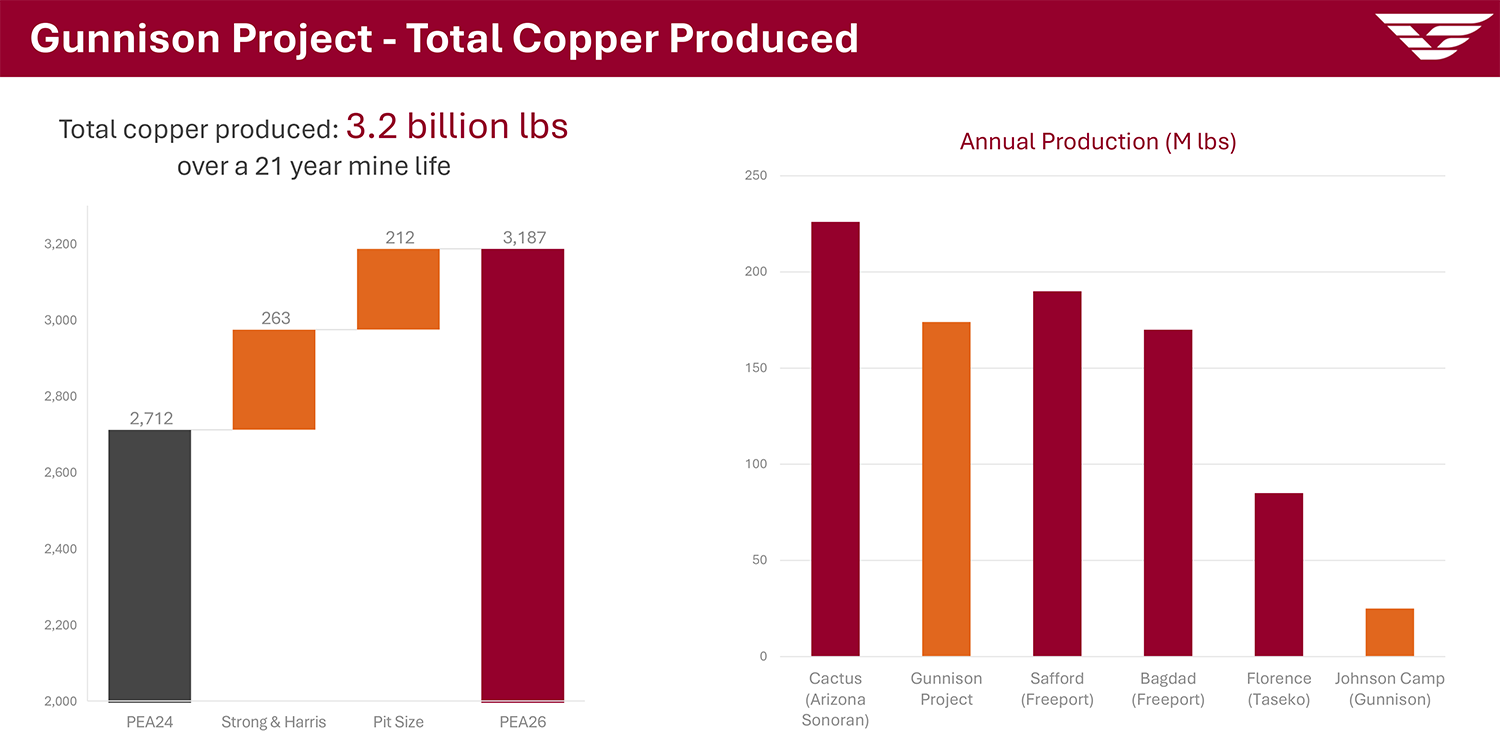

Johnson Camp sits adjacent to the larger Gunnison Project, hosting over 846 million tons at approximately 0.33% copper in Measured & Indicated resources (Measured Mineral Resource of 191.5 million tons at 0.37% and Indicated Mineral Resource of 654.5 million tons at 0.31%) and an updated 2026 PEA outlining significantly improved economics: US$2.0B NPV (8%), 23% IRR, and a 3.9-year payback period.

The PEA is preliminary in nature and includes Inferred Mineral Resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves. There is no certainty that the conclusions reached in the PEA will be realized. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability.

Gunnison Copper’s flagship Gunnison Project continues to advance following the completion of its High-Value-Add Work Program, which delivered strong metallurgical and ore-sorting results that improve recoveries, grades, and costs. The company is now advancing the Gunnison Project toward a Pre-Feasibility Study (PFS) following the release of the updated 2026 PEA.

Assuming Gunnison is permitted, financed, constructed and reaches full production, the project has the potential to supply up to 8% of America’s total copper demand, positioning it as one of the nation’s most strategic open-pit, heap-leach copper developments.

Together, JCM and the Gunnison Project form the foundation of a true district-scale growth platform — with Rio Tinto’s Nuton® technology positioned to unlock the sulfide potential and drive the next phase of expansion.

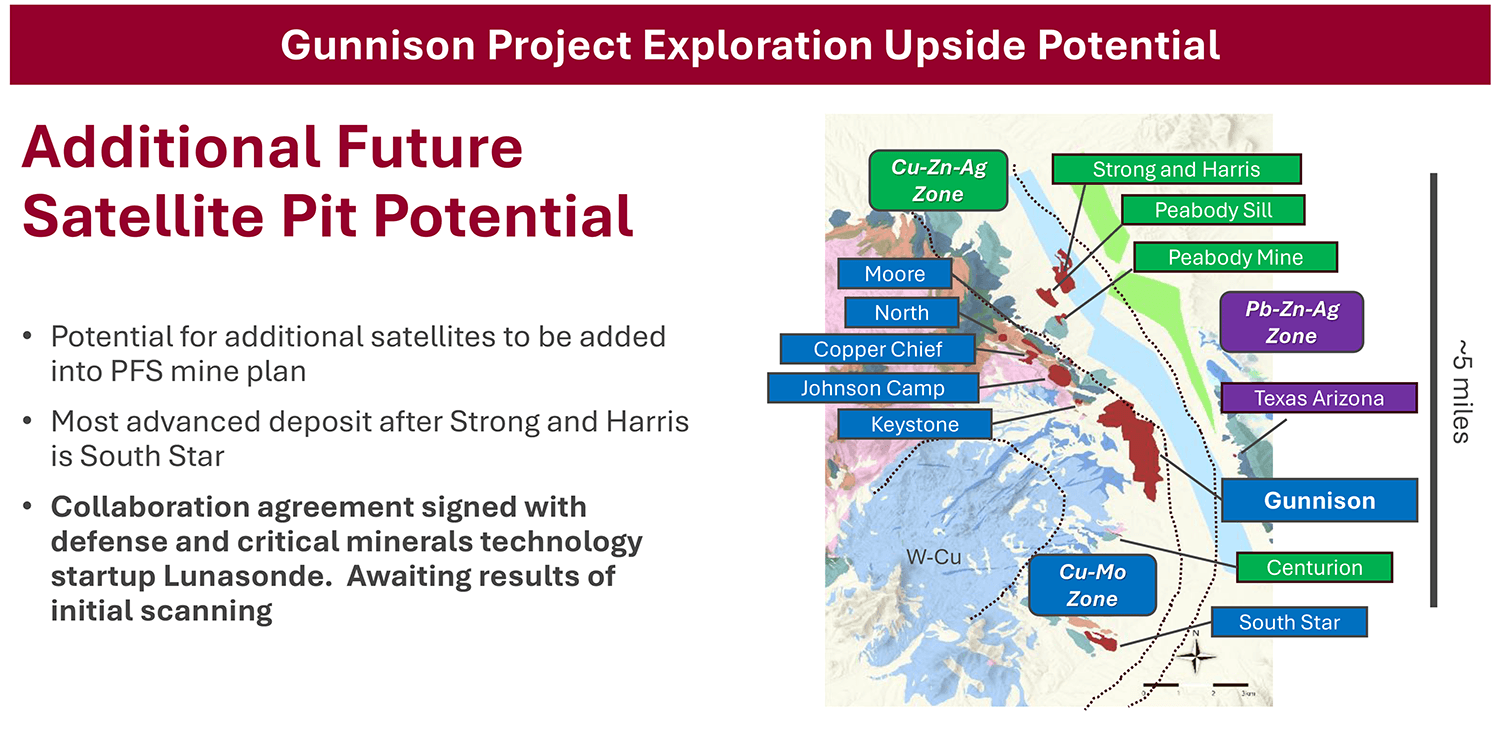

The district also holds several satellite deposits — South Star, and more — that could ultimately feed the Gunnison Project’s future infrastructure.

Simply put, the Johnson Camp Mine is a growth platform very few juniors ever achieve: production today, fully financed production supported by a global major, and total district-scale control in one of the safest mining jurisdictions on the planet.

Yet this story doesn’t stop with first production and district control. With Nuton® now deployed at industrial scale, the next chapter is already underway.

Innovation Beyond Nuton®:

Lunasonde Partnership Adds Exploration Upside

Next-Gen Subsurface Imaging Aims to Unlock New Discoveries

While Nuton® is now being deployed at industrial scale, Gunnison is also looking ahead to the next frontier of exploration.

![]()

The company has partnered with Tucson-based defense-tech startup Lunasonde Inc. to deploy its airborne georadiotomography (aGRT) platform across portions of the Cochise Mining District.

Gunnison recently announced that Lunasonde has now completed its airborne survey program with data processing currently underway and initial results expected in the near term.

Adapted from space exploration technology used to scan beneath the surface of planets and asteroids, Lunasonde’s system is being applied to help identify potential copper-bearing structures hidden beneath Arizona’s extensive alluvial cover.

Gunnison plans to integrate the incoming data with its existing geological and geophysical datasets to prioritize high-potential drill targets and support potential resource expansion opportunities across the broader district-scale land package.

The collaboration also aligns with broader US efforts to strengthen domestic critical mineral supply chains, particularly in support of defense, manufacturing, AI infrastructure, and advanced technologies.

If successful, the partnership adds another layer of exploration upside to Gunnison’s already expansive Cochise Mining District platform — positioning the company not just as America’s newest copper producer but also as an early adopter of advanced technologies aimed at unlocking the next generation of domestic mineral discoveries.

The Red Metal in a Global Squeeze

Soaring Prices, Fragile Supply Chains, and Historic Demand

Copper — known as the red metal — sits at the heart of the global economy.

From EVs and AI data centers to energy grids and national defense, there is no path to growth or security without it. That’s why the price has surged above US$6/lb with analysts pointing to further upside as supply shocks ripple through the market.

One of the most dramatic reminders of that fragility came recently when a catastrophic mud rush struck Freeport-McMoRan’s Grasberg Mine in Indonesia — the world’s second-largest copper operation.

With output now expected to remain 35% lower through at least 2026, the disruption has tightened an already strained market and pushed copper to multi-month highs.

Layer on demand from electrification, reindustrialization, and a broader commodity supercycle lifting gold, silver, and copper together — and it’s clear why copper is drawing comparisons to oil in terms of strategic importance.

The US government itself is leaning hard into reshoring supply with billions in tax credits and funding programs designed to incentivize domestic production.

Against this backdrop, Gunnison Copper’s emergence as America’s newest copper producer couldn’t be better timed.

As Craig Hallworth recently noted,

“A single big data center could use one or two million pounds of copper… and we’re going to need a lot of copper to make sure the United States stays number one in artificial intelligence.”

Adding further credibility to Gunnison’s growing strategic importance, the company was recently granted membership into the Defense Industrial Base Consortium (DIBC) — a US Department of Defense-sponsored initiative focused on strengthening domestic supply chains for critical minerals and industrial technologies tied to national security.

The invitation-only consortium provides Gunnison potential access to non-dilutive funding opportunities, strategic partnerships, and government-backed programs designed to accelerate US-based copper production capacity.

As Hallworth explained regarding the milestone:

“Membership in the DIBC marks an important milestone for Gunnison as we continue to position ourselves as a reliable, scalable, domestic source of copper for US defense and manufacturing supply chains. Our ability to rapidly deliver new production, combined with the significant scale of our development pipeline, positions Gunnison to benefit from potential government-backed funding and to accelerate development of our projects while supporting critical US supply chains.”

The company is already well on its way to meeting that demand — producing today, ramping production at JCM, and preparing for a potential step-change with Rio Tinto’s Nuton® technology.

For speculators, that means exposure to one of the purest Made-in-America copper stories just as the red metal enters what may be its most important cycle in decades.

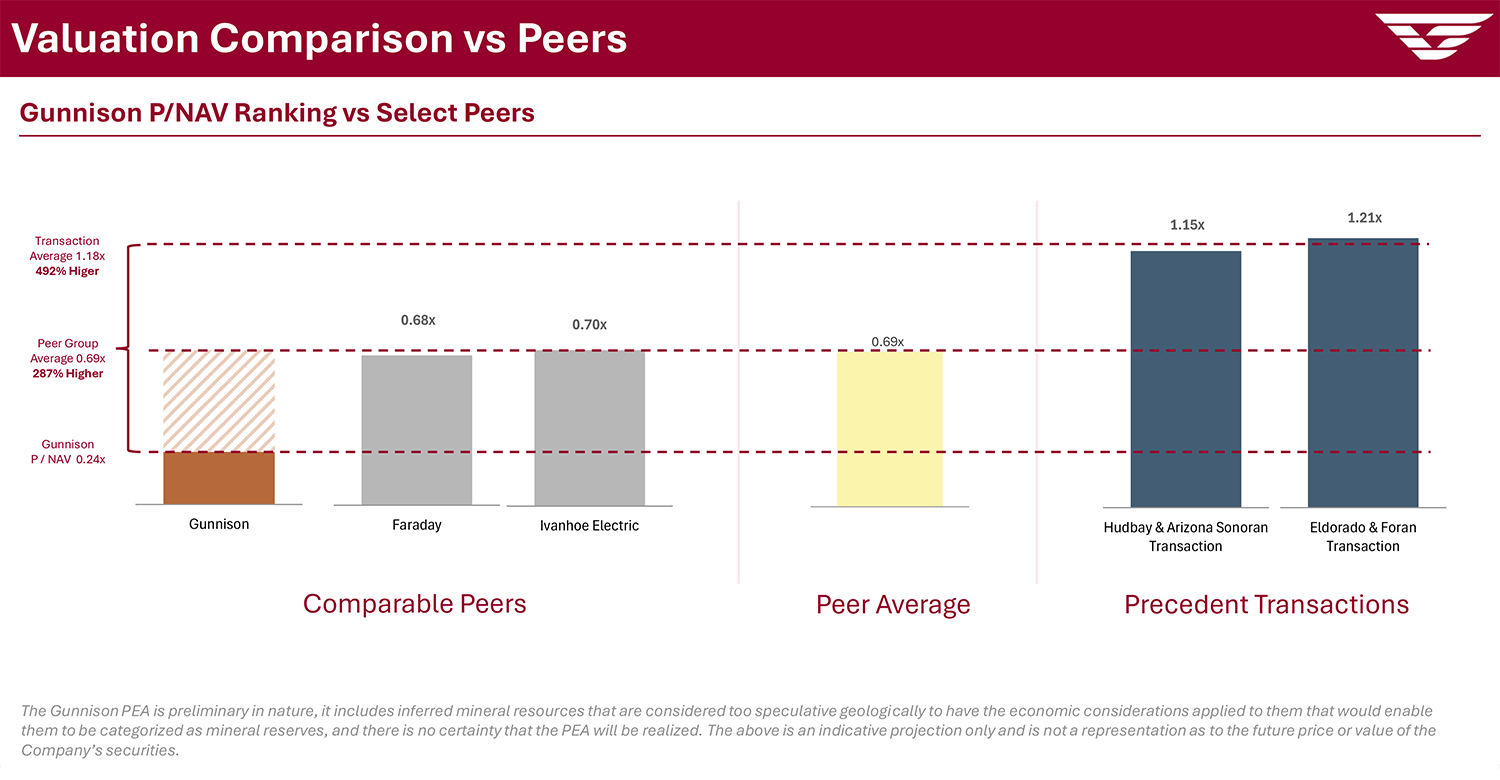

Peer Comparisons Highlight the Valuation Gap

Arizona Copper Producers Command $Billions

— Gunnison Still Under US$130M

When it comes to copper in Arizona, the market has already assigned premium valuations to established players.

Gunnison Copper is already producing and selling copper from its Johnson Camp Mine — yet the company’s market cap remains under ~US$130M despite recent operational, financial, and economic milestones.

This valuation gap persists even after the company eliminated its Nebari secured debt, deployed Nuton® technology at industrial scale, and released an updated 2026 PEA outlining materially improved project economics.

Craig Hallworth underscores the point:

“Right now, our price-to-NAV is about 0.15. Our peers in Southern Arizona are trading around 0.45.”

Next, Gunnison Copper CEO Craig Hallworth explains why the company remains significantly undervalued despite its growing role as one of America’s most strategically important new copper producers.

Exclusive Interview with Gunnison Copper

CEO Mr. Craig Hallworth

We already introduced you briefly to the leadership team behind Gunnison Copper — but it’s worth underscoring the caliber of professionals driving this story forward.

At the helm is newly promoted President & CEO Craig Hallworth who continues to play a central role in shaping Gunnison’s financial strategy, key partnerships, and production growth strategy.

Supporting operations in the field is COO Robert Winton, P.Eng.. Winton brings deep technical expertise and a strong operational background, and his focus on efficiency, ESG practices, and innovative technologies like Nuton® ensures Gunnison is building production the right way.

Also remaining closely involved with the company is Dr. Stephen Twyerould, now serving as a Director of Gunnison Copper. A seasoned mine builder with more than three decades of experience advancing copper, gold, and uranium projects globally, Twyerould continues to provide strategic guidance as Gunnison advances its district-scale Arizona copper platform.

Next, Hallworth — the voice you’ll hear directly in our exclusive interview — discusses the company’s updated PEA, growing strategic importance to US supply chains, and the roadmap ahead for Gunnison Copper.

Gerardo Del Real: This is Gerardo Del Real with Resource Stock Digest. Joining me today is the newly promoted CEO of Gunnison Copper (TSX: GCU)(OTC: GCUMF) — Mr. Craig Hallworth. Craig, how are you today?

Craig Hallworth: Hi, Gerardo. I'm doing well. Great to be here.

Gerardo Del Real: Well, listen, let's get right to it. There’s a lot to dig into. You’ve had, I would say, some good fortune — but frankly, it’s been excellent execution. You’ve benefited from ~US$6/lb copper, which we’re right on the cusp of again, and you’ve been executing brilliantly.

Back a few weeks ago, you had a PEA that was filed. Congrats on that. And I want to dig into the details there, but I’ve got to start with the news this morning, because it's rare in 2026 that there's actually bipartisan support for much in this country.

You were just accepted into the US Defense Industrial Base Consortium, the DIBC, which is a government-backed initiative focused on strengthening domestic supply chains for critical minerals and technologies that are essential to national security. That is a big get for a company with what I’ll say is a market cap that has a lot of catching up to do.

I’d like to start there, and then hopefully you can give me some guidance on what this means for the company and what it means moving forward.

Craig Hallworth: You're right, Gerardo. This is a big boost at Gunnison Copper. If you look at our mission statement, we exist to develop, advance, and produce copper in Arizona, in the United States. And we’re selling that. We’re selling it right now into the supply chains from our Johnson Camp Mine and soon from our Gunnison Copper Project.

We’re looking to supply defense. We’re looking to supply manufacturing. So it’s a great fit for us — the Defense Industrial Base Consortium. This is an invitation-only grouping of American companies. It’s backed by the Department of Defense. What they’re seeking to do is to really advance and scale the domestic supply chains — the industrial base, if you will.

It’s badly needed right now. We’re in a very uncertain world. If you look around the world — the tensions, the geopolitics — there’s conflict, and we need to have a strong military. We need to have munitions. Munitions are being depleted across the board, and those munitions need to be replenished.

If you look at the scale of the munitions — say, the Ukraine war and just how many drones are being built — we’re talking millions. And all of those drones need copper. And so do ammunition components, and so do rockets, and so does artillery. So everything needs copper. It’s one of the most used metals in defense.

That’s where Gunnison Copper comes in. That’s how we can help this country strengthen the supply chain. We hope to work with the Department of Defense to accelerate our Gunnison Copper Project.

It’ll be able to make something like 174 million pounds of copper a year, or even perhaps more with some optimization. And that’s going to be a material, national-level impact on the industrial supply base in this country.

Gerardo Del Real: Being a 100% Made-in-America copper producer and developer, I’ve got to believe that with the acceptance into the DIBC, it’s probably going to give you access to a lot of perks that a lot of companies are going to be envious of. And I know one of those has to be the potential for non-dilutive funding moving forward.

Craig Hallworth: Absolutely. That’s one of our main objectives here. You mentioned our market capitalization. We’re something like a C$200 million market cap today. The Gunnison Project — the CapEx for that — is going to be about $1.5 billion, and that’s because it’s a project with scale.

And like you said, it’s going to make finished copper in the United States. Over 50% of the copper we consume today — and that includes the defense sector in this country — is coming from foreign sources. And that’s not including all of the growth that’s projected.

Everyone knows there’s incredible growth coming in copper. When I talk to portfolio managers, when I talk to fund managers, when I talk to institutions, they are all extremely constructive on copper because they see the growth that’s coming. So that deficit, in terms of secure supply made in-country, is only going to get bigger.

This is part of our motivation here for joining this consortium — access to government capital. If you take a look at our project, if you take a look at the CapEx, and if you take a look at the available government capital, there is a US$100 billion fund that has been earmarked for accelerating domestic critical mineral projects, just like the Gunnison Copper Project.

I think it is a good partnership potential for us. I think it aligns with our values. We want to supply the defense sector. And in fact, we are supplying the defense sector, because we’re supplying Amazon Web Services, and they have extensive government contracts and cloud computing across the defense space.

We’re already supplying the defense sector, and we are eager to do more. And I think partnering with the government makes a whole lot of sense here.

Gerardo Del Real: Look, it's a heck of an endorsement, given the fact that the PEA that was filed demonstrates an after-tax net present value using a base copper price of US$4.60/lb. We're pushing US$6/lb, and anyone paying attention to the space has a pretty good inclination of seeing much higher prices here in the mid to long-term.

Can you speak to the PEA that was filed and then some of the highlights there?

Craig Hallworth: We're getting a lot of feedback from all over the country. People are impressed with this study. They're saying this is a large project, it's got scale, and the grade compares very favorably with the big mines that are being mined in Arizona today.

We're leaching, on a total copper basis, 0.43% total copper. If you look at Freeport, if you look at ASARCO — those big companies with the big open pits in production today — they're typically under 0.3%. So we're at about a 50% higher grade at our project versus those big mines in operation today.

We were able to add in one of our satellite deposits — it's called Strong and Harris — and that deposit has a grade of 0.85% total copper. So that's triple the grade of these big mines in production today.

When people look at the project, they say, ‘This thing’s got scale — it’s going to make 174 million pounds a year.’ That’s about 11% of current US refined copper production from mined ore today. So this thing is going to move the needle for the country. It's got a very good grade, and we were able to really increase the total metal produced as well.

We increased from 2.7 billion pounds of copper in the ground that we're going to mine and turn into finished product to 3.2 billion pounds. So that's an increase of 500 million pounds.

That's what people want to see. Investors want to see metal increase. That's the number one thing. I mean, after all, that's why we're in business, right? We're in business to build a mine that makes copper. And when we talk about making copper — the more copper, the merrier.

We worked hard as a team. We worked all year. Let’s add as much metal to this thing as we can. And part of that came from including this satellite deposit, Strong and Harris, and the other half of that increase in metal came from optimizations we were able to do to the main pit — the main Gunnison pit.

We’re really excited about the study. Everyone says it looks great, and investors are very happy with the improvements that were made over the previous study.

Gerardo Del Real: The million-dollar question as always, Craig — what comes next? Impressive work, obviously, and you've clearly been very busy behind the scenes, but what comes next?

Craig Hallworth: We are now gearing up for our Pre-Feasibility Study. And in fact, we're going to start metallurgical testing this month.

We've got a work program that we've created. We're going to be coming to the market very soon — in the next few weeks — to let everybody know all of the details.

What are we going to be doing? What is the metallurgical testing program we're going to be doing? What is the infill drill program we're going to be doing to upgrade all of the resources to get us to a reserve? What’s the path on the engineering to advance that? Is there exploration drilling?

The answer, I believe, is going to be yes, because we think that we can add a lot more tonnes to Strong and Harris. This is the satellite deposit — the very high-grade deposit I mentioned earlier — and I believe we'll be able to add a lot more tonnes to that. But that requires some exploration drilling, so we're going to have that in our budget.

On top of that is finally the most important part, which is our permit amendments. What's the plan for the permit amendments? How are we going to get those permits amended? What’s our strategy? What are all the details? Who’s going to do it?

You're going to hear all about that in the coming weeks. So please follow us at our website. Watch for our news releases. You're going to hear about the detailed work program, and we're going to be delivering catalysts from that in the next 3, 6, 12, and 24 months.

It's not going to be all saved up for the end in two years. When we execute our intended plan to go to market with that PFS study — with the reserve and with the permits amended — there are going to be big things happening all the way through, and you'll need to keep watching our news releases for those details.

Gerardo Del Real: Well, the acceptance into the DIBC, I think, is also going to give you some flexibility you previously didn’t have. Great work, Craig, all the way around. Looking forward to having you back on and catching up soon.

Craig Hallworth: Thank you for having me, Gerardo.

The Gunnison Copper Opportunity

Gunnison Copper Corp. (TSX: GCU)(OTCQB: GCUMF) has emerged as America’s newest copper producer — delivering first production from the fully operational Johnson Camp Mine in southeastern Arizona.

At the core is a district-scale platform: Gunnison controls a large portion of the Cochise Mining District, encompassing 12 known deposits within an 8 km corridor.

Production from Johnson Camp is underway — with a nameplate capacity of 25 million pounds annually — with every pound mined and processed within the United States.

Gunnison currently trades at a market cap below US$130M — just a fraction of what established Arizona copper producers are worth — despite already producing and selling copper mined, processed, and delivered entirely in America.

As Gunnison’s Craig Hallworth recently noted:

“We’re selling copper right now into the supply chains from our Johnson Camp Mine and soon upcoming from our Gunnison Copper Project. We’re looking to supply defense, we’re looking to supply manufacturing — and that’s exactly where Gunnison fits.”

The company’s financial position underpins this growth trajectory.

On 30 October 2025, GCU closed a non-brokered private placement for gross proceeds of C$13.1 million, consisting of 29.1 million units priced at C$0.45 per unit. Funds will be directed toward drilling, metallurgical testing, and permitting activities to support the Pre-Feasibility Study for the Gunnison Copper Project.

More recently, Gunnison also secured a new C$30 million bought-deal financing led by Canaccord Genuity, further strengthening the company’s balance sheet as it advances production ramp-up and Pre-Feasibility Study activities.

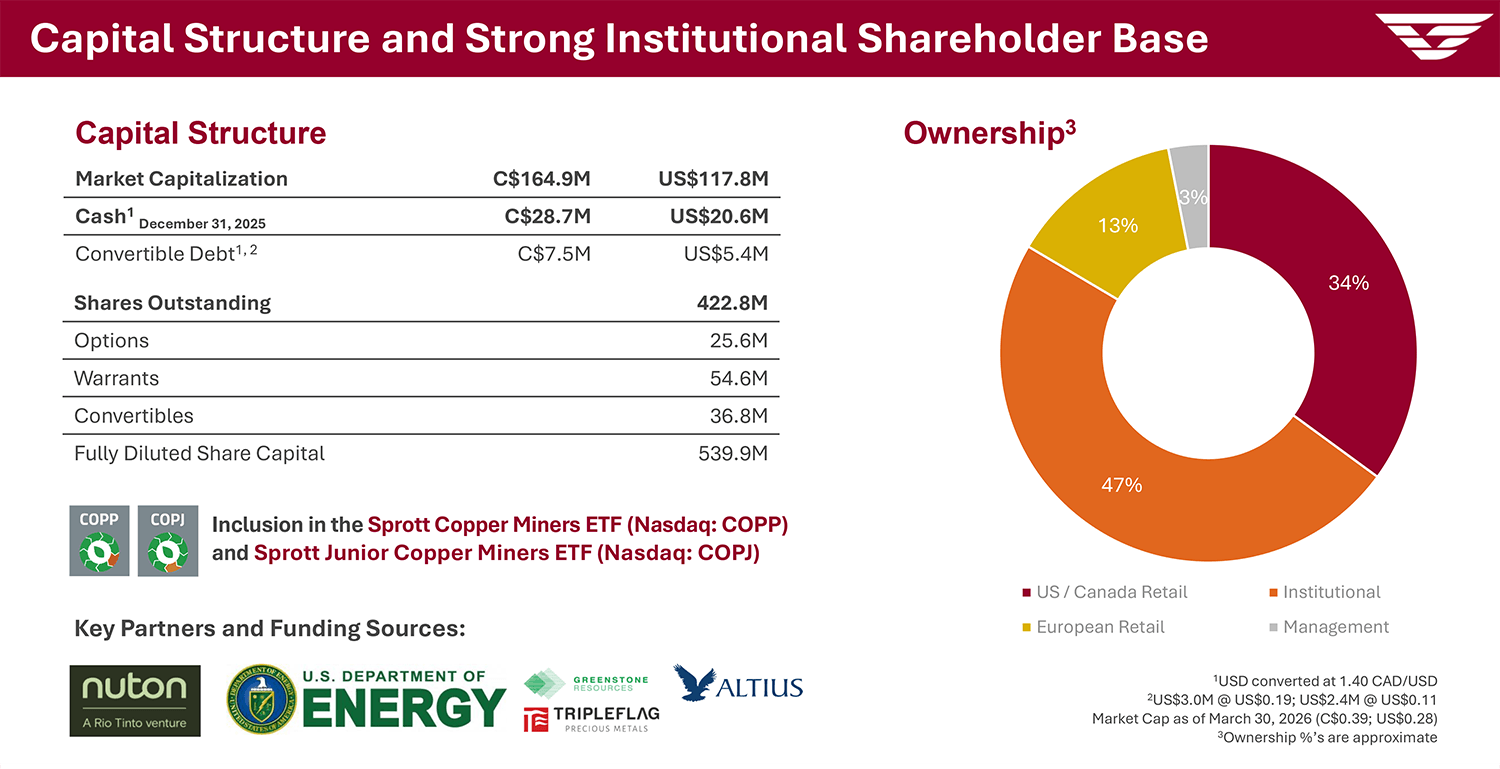

With ~422.8M shares outstanding (~539.9M fully diluted) and a treasury of ~US$20.6M as of December 31, 2025, Gunnison is well funded to advance its growth initiatives.

In January 2026, Gunnison achieved a major balance sheet milestone by fully eliminating all outstanding Nebari debt, reducing the principal from US$15 million to zero and strengthening the company’s financial position as it advances toward development of the flagship Gunnison Project.

Additionally, Gunnison has secured approval under the Arizona Commerce Authority’s Qualified Facility Tax Credit Program, providing the company with an additional source of non-dilutive state-backed funding tied directly to copper manufacturing and job creation in Arizona.

Complementing those balance sheet milestones, GCU also reported preliminary findings from an independent Economic Impact Study conducted by the University of Arizona’s Eller Partnerships Office on the Gunnison Copper Project.

The study projects total US economic output of ~US$14B over the life of the project, supporting more than 53,000 job-years, and generating ~US$2B in labor income.

The study reinforces the project’s potential to become a nationally significant source of Made-in-America copper while delivering meaningful long-term economic impact across Arizona and the broader US supply chain.

While not a feasibility analysis, the report highlights the project’s transformative scale and long-term importance to Arizona and US manufacturing supply chains.

Recent admission into the US Defense Industrial Base Consortium (DIBC) further reinforces GCU’s growing strategic importance as a domestic copper supplier tied to critical US manufacturing, infrastructure, AI, and national security initiatives.

With copper surging beyond US$6/lb, global supply shocks from Indonesia’s Grasberg Mine, and government-backed incentives like US$13.9M in DOE tax credits already awarded (subject to final certification) — the timing couldn’t be better.

Currently trading just below Wall Street’s radar around US$0.30 per share, the opportunity is clear: early entry into a company already producing, scaling up, and backed by one of the world’s biggest copper players.

With recent milestones including entry into the DIBC, industrial-scale deployment of Nuton® technology, and Johnson Camp copper entering the Amazon Web Services supply chain, GCU is increasingly aligned with some of the most important domestic demand drivers in the market today.

For speculators, Gunnison Copper represents one of the more compelling Made-in-America copper growth stories in the small-cap space today.

To continue your due diligence, please visit Gunnison Copper’s corporate website to explore the projects, meet the team, and sign up for direct updates.

View the most recent Corporate Presentation here.

Gunnison Copper Corp. trades on the TSX under the symbol GCU, on the OTCQB under the symbol GCUMF, and in Frankfurt under the symbol 3XS0.

— Resource Stock Digest Research

Click here to see more from Gunnison CopperThe PEA is preliminary in nature and includes Inferred Mineral Resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves. There is no certainty that the conclusions reached in the PEA will be realized. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability. For additional information on the Gunnison Project, including the PEA and mineral resource estimate, please refer to the Company's technical report entitled "Gunnison Project NI 43-101 Technical Report Preliminary Economic Assessment" available on SEDAR+ at www.sedarplus.ca.

Dr. Stephen Twyerould, Fellow of AUSIMM, Director of the Company is a Qualified Person as defined by NI 43-101. Dr. Twyerould has reviewed and is responsible for the technical information contained in this report.

Certain statements contained in this release constitute forward-looking information within the meaning of applicable Canadian securities laws. Such forward-looking statements relate to the intention to deploy the Nuton® technology at the Johnson Camp mine and future production therefrom; the continued funding of the stage 2 work program by Nuton; the details and expected results of the stage two work program; future production and production capacity from the Company's mineral projects; the results of the preliminary economic assessment on the Gunnison Project; expected future production; details regarding plans for a prefeasibility study; and the exploration and development of the Company's mineral projects.

In certain cases, forward-looking information can be identified by the use of words such as "plans", "expects" or "does not expect", "budget", "scheduled", "estimates", "forecasts", "intends", "anticipates" or "does not anticipate", or "believes", or variations of such words and phrases or state that certain actions, events or results "may", "could", "would", "might", "occur" or "be achieved" suggesting future outcomes, or other expectations, beliefs, plans, objectives, assumptions, intentions or statements about future events or performance. Forward-looking information contained in this report is based on certain factors and assumptions regarding, among other things,Nuton will continue to fund the stage 2 work program, the availability of financing to continue as a going concern and implement the Company's operational plans, the estimation of mineral resources, the realization of resource and reserve estimates, copper and other metal prices, the timing and amount of future development expenditures, the estimation of initial and sustaining capital requirements, the estimation of labour and operating costs (including the price of acid), the availability of labour, material and acid supply, receipt of and compliance with necessary regulatory approvals and permits, the estimation of insurance coverage, and assumptions with respect to currency fluctuations, environmental risks, title disputes or claims, and other similar matters. While the Company considers these assumptions to be reasonable based on information currently available to it, they may prove to be incorrect.

Forward-looking information involves known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the Company to be materially different from any future results, performance or achievements expressed or implied by the forward-looking information. Such factors include risks related to the Company not obtaining adequate financing to continue operations, Nuton failing to continue to fund the stage 2 work program, the breach of debt covenants, risks inherent in the construction and operation of mineral deposits, including risks relating to changes in project parameters as plans continue to be redefined including the possibility that mining operations may not be sustained at the Gunnison Copper Project, risks related to the delay in approval of work plans, variations in mineral resources and reserves, grade or recovery rates, risks relating to the ability to access infrastructure, risks relating to changes in copper and other commodity prices and the worldwide demand for and supply of copper and related products, risks related to increased competition in the market for copper and related products, risks related to current global financial conditions, risks related to current global financial conditions on the Company's business, uncertainties inherent in the estimation of mineral resources, access and supply risks, risks related to the ability to access acid supply on commercially reasonable terms, reliance on key personnel, operational risks inherent in the conduct of mining activities, including the risk of accidents, labour disputes, increases in capital and operating costs and the risk of delays or increased costs that might be encountered during the construction or mining process, regulatory risks including the risk that permits may not be obtained in a timely fashion or at all, financing, capitalization and liquidity risks, risks related to disputes concerning property titles and interests, environmental risks and the additional risks identified in the "Risk Factors" section of the Company's reports and filings with applicable Canadian securities regulators.

Although the Company has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking information, there may be other factors that cause actions, events or results not to be as anticipated, estimated or intended. Accordingly, readers should not place undue reliance on forward-looking information. The forward-looking information is made as of the date of this report. Except as required by applicable securities laws, the Company does not undertake any obligation to publicly update or revise any forward-looking information.

IMPORTANT DISCLAIMER & DISCLOSURES

Resource Stock Digest, as a publisher, is not a broker, investment advisor, or financial advisor in any jurisdiction.

Please do not rely on the information presented by Resource Stock Digest as personal investment advice.

If you need personal investment advice, kindly reach out to a qualified and registered broker, investment advisor, or financial advisor.

The communications from Resource Stock Digest should not form the basis of your investment decisions. Examples we provide regarding share price increases related to specific companies are based on randomly selected time periods and should not be taken as an indicator or predictor of future stock prices for those companies.

Gunnison Copper has sponsored this report.

The information in this newsletter does not constitute an offer to sell or a solicitation of an offer to buy any securities of a corporation or entity, including U.S. Traded Securities or U.S. Quoted Securities, in the United States or to U.S. Persons. Securities may not be offered or sold in the United States except in compliance with the registration requirements of the Securities Act and applicable U.S. state securities laws or pursuant to an exemption therefrom.

Any public offering of securities in the United States may only be made by means of a prospectus containing detailed information about the corporation or entity and its management as well as financial statements. No securities regulatory authority in the United States has either approved or disapproved of the contents of any newsletter. Neither Resource Stock Digest nor any employee of Resource Stock Digest is registered with the United States Securities and Exchange Commission (the “SEC”): as a “broker-dealer” under the Exchange Act, as an “investment adviser” under the Investment Advisers Act of 1940, or in any other capacity. Resource Stock Digest, its owners, directors, and employees are also not registered with any state securities commission or authority as a broker-dealer or investment advisor or in any other capacity.

HIGHLY BIASED:

In our role, we aim to highlight specific companies for your further investigation; however, these are not stock recommendations, nor do they constitute an offer or sale of the referenced securities. Resource Stock Digest has received cash compensation from Gunnison Copper and is thus extremely biased. It is crucial that you conduct your own research prior to investing. This includes reading the companies' SEDAR and SEC filings, press releases, and risk disclosures. The information contained in our profiles is based on data provided by the companies, extracted from SEDAR and SEC filings, company websites, and other publicly available sources.

Resource Stock Digest, and its owners, directors, employees, and members of their households may own shares of Gunnison Copper. Therefore, Resource Stock Digest is extremely biased. Measures are in place such that no shares will be sold during the active awareness campaign.

HIGH RISK:

The securities issued by the companies we feature should be seen as high risk; if you choose to invest, despite these warnings, you may lose your entire investment. You must be aware of the risks and be willing to accept them in order to invest in financial instruments, including stocks, options, and futures.

NOT PROFESSIONAL ADVICE:

By reading this, you agree to all of the following: You understand this to be an expression of opinions and NOT professional advice. You are solely responsible for the use of any content and hold Resource Stock Digest, and all partners, members, and affiliates harmless in any event or claim. While Resource Stock Digest strives to provide accurate and reliable information sourced from believed-to-be trustworthy sources, we cannot guarantee the accuracy or reliability of the information. The information provided reflects conditions as they are at the moment of writing and not at any future date. Resource Stock Digest is not obligated to update, correct, or revise the information post-publication.

FORWARD-LOOKING STATEMENTS:

Certain information presented may contain or be considered forward-looking statements. Such statements involve known and unknown risks, uncertainties, and other factors that may cause actual results or events to differ materially from those anticipated in these statements. There can be no assurance that any such statements will prove to be accurate, and readers should not place undue reliance on such information. Resource Stock Digest does not undertake any obligations to update the information presented or to ensure that such information remains current and accurate.